Welcome back everyone. Have you been pouring over your open enrollment options? Well, lets add another pot to the stove as we look at Medicare Part D.

What is Medicare Part D?

Medicare Part D was enacted as part of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (MMA) and went into effect on January 1, 2006. Before this time, there was NO prescription drug coverage affiliated with Medicare. Most Medicare recipients purchased private drug plans or got drug coverage through their Medicare Advantage plan. Lower income individuals received assistance through state programs for the elderly and disabled. However, many Medicare recipients had no prescription coverage at all prior to the implementation of Part D.

What does it cost?

There are out of pocket costs at many different levels with Medicare part D. First, you will pay a monthly premium for your coverage. Most drug plans charge a monthly fee that varies by plan. You pay this in addition to the Part B premium. If you belong to a Medicare Advantage Plan (like an HMO or PPO) or a Medicare Cost Plan that includes Medicare prescription drug coverage, the monthly premium you pay to your plan may include an amount for prescription drug coverage. Furthermore, your costs are influenced by the following:

- The prescriptions you use and whether your plan covers them

- The plan you choose

- Whether you go to a pharmacy in your plan’s network

- Whether your drugs are on your plan’s formulary

- Whether you get Extra Help paying your Part D costs

There are also out of pocket expenses (co-pays or cost sharing) for your prescriptions.

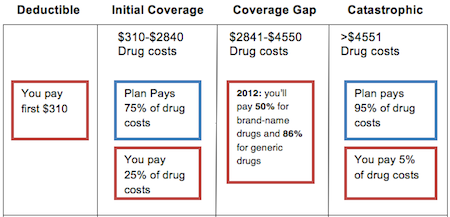

Here is a chart to help us visualize:

More about the coverage gap; aka “the donut hole”

The coverage gap or “donut hole” as it is more popularly known, is undergoing some major changes over the next several years, with the goal being to close the donut hole by 2020. In 2012, the plans will be offering more savings, including coverage of 50% of the costs of brand name and 86% of the cost of generic drugs. This only applies if you are NOT receiving “extra help” (see more about this below) and are already in the coverage gap. You reach the donut hole when you and the drug insurance plan have paid $2850 for medications. You are in the donut hole until the total amount paid for medications is $4550. At this point you will enter the catastrophic coverage period. These levels reset EVERY year on January 1st – i.e. you start accruing costs all over again.

What is covered?

It’s important to shop around when considering a part D plan. The Medicare website, medicare.gov, allows you to enter all the medications you are taking and research the costs of drugs with various plans. Different Medicare Part D plans may cover different drugs. Each plan has its own “formulary”. A formulary is a list of drugs covered by a plan and the cost under that one plan. Most Medicare drug plans operate under a “tiered” system. Drugs in each tier have different costs. A drug in a lower tier will have a lower cost than one in a higher tier. If your doctor advises a drug on a higher tier rather than a similar drug on a lower tier you may be able to file an exception and get a lower copayment. Often you have to “fail” therapy on a lower tier BEFORE the drug company will approve the drug at a higher tier.

What is not covered?

There are also certain classes of drugs that are excluded in Part D, including:

- Fertility drugs

- Drugs for weight gain, weight loss, or for treating anorexia

- Drugs for treating erectile dysfunction

- Cosmetic drugs

- Cough and cold suppressants

- Benzodiazepines

- Barbiturates

- Vitamins and minerals except prenatal vitamins

Special information for cancer patients about oral chemotherapy drug coverage

Certain chemotherapy drugs have an IV equivalent:–i.e. if your doctor has a choice between giving you an oral drug or the same drug as an IV, the oral drug is covered under Part B. In comparison, oral cancer drugs that cannot be given as an IV are covered under Part D, not Part B. Oral chemotherapy drugs covered under part B include Xeloda, Busulfan, Melphalan and Etoposide. If you are receiving one of these medications, you will be responsible for 20% of the cost (as with other part B expenses) unless you have a secondary (Medigap) plan (see previous blog entries for more about this).

Other oral chemotherapy drugs are extremely costly. With some of these drugs, you will be in the “donut hole” after one month of therapy. It is important to work closely with your physician and social worker if you have having trouble paying for the cost of these medications as sometimes help is available through the pharmaceutical company and co-pay assistance foundations.

Where can I get help paying for my medications?

The government (Social Security Administration) does offer assistance for lower income individuals through the low income subsidy/extra help program. Medicare beneficiaries can qualify for Extra Help with their Medicare prescription drug plan costs. You may qualify for extra help if:

- You have Medicare Part A (Hospital Insurance) and/or Medicare Part B (Medical Insurance); and

- You live in one of the 50 states or the District of Columbia; and

- Your combined savings, investments, and real estate are not worth more than $25,260, if you are married and living with your spouse, or $12,640 if you are not currently married or not living with your spouse. (Does not include the home you live in, vehicles, personal possessions, burial plots, irrevocable burial contracts or back payments from Social Security or SSI.)

If you do not qualify for extra help, you may be eligible for state assistance, (for example PACE/PACEnet in Pennsylvania or PAAD in New Jersey) depending on where you live. To find out more about what programs your state may offer see http://www.medicare.gov/pharmaceutical-assistance-program/state-programs.aspx.

What if I don’t enroll?

Of course it is your choice to enroll in Part D coverage, but if you opt out, you will be responsible for all out of pocket drug costs. Also, some pharmaceutical sponsored patient assistance programs will not approve patients for assistance if they have opted out of coverage (i.e. chosen to be underinsured when an option was available). Also, if you do not enroll when you are first eligible for Medicare, you may be assessed penalties for late enrollment in part D. This penalty is added on to your monthly premium costs already deducted from your Social Security. To estimate the penalty, find the national base beneficiary premium for the year ($30.36 in 2009, $31.94 in 2010) and take 1% of that ($.30 in 2009, $0.32 in 2010). Multiply it by the number of uncovered, full calendar months (during any continuous period of 63 days or more), since the end of your initial enrollment period (IEP), during which you did not have creditable coverage. Take the answer and round it to the nearest 10 cents. This amount will be added to your plan’s premium amount even if the plan’s premium is $0. Your penalty will change each year that the national average premium changes.

For example, Suzy was eligible for Medicare coverage beginning in January of 2008. Suzy elected not to have Medicare Part D Coverage. During open enrollment for 2012, Suzy decides she does want to have Part D coverage. She was uncovered for a total of 4 years or 48 months. If the base beneficiary premium is $32.00, 1% of this is .32. We multiply this times 48 which equals $15.36. This would be the monthly penalty assessed to Suzy for LIFE for her delayed enrollment in Part D. (https://questions.medicare.gov/app/answers/detail/a_id/2255/~/late-enrollment-penalty-%28lep%29)

Still need help deciding what plan works for you?

Log on to our webchat, Making Medicare Work For YOU! on Tuesday November 8th from 12-1 pm and utilize the resources available via 1-800-MEDICARE and medicare.gov

Next week I’ll focus on copay assistance programs and how these can help minimize your financial burden while dealing with cancer.